Driving in Michigan comes with its own unique set of rules for auto insurance, primarily because it’s a no-fault state. This means every driver is required to carry specific coverages: Personal Injury Protection (PIP), Property Protection Insurance (PPI), and Bodily Injury/Property Damage Liability (BI/PD). Understanding these three mandatory coverages is the first step to ensuring you are legally and safely covered on Michigan roads.

Navigating Michigan’s Unique Insurance Landscape

Michigan’s approach to car insurance is different from that of most other states. The system is built around the “no-fault” concept, meaning that if you are in an accident, your own insurance policy is the primary source for covering your medical bills, regardless of who was at fault. The intent of this system is to ensure injury claims are paid promptly without lengthy legal disputes.

Because of this structure, the Michigan auto insurance requirements are very specific and mandatory for all drivers. Operating a vehicle without the required coverage can lead to serious legal consequences, including fines, license suspension, and even potential jail time. To comply with state law, your policy must include three core components designed to protect you and others on the road.

The Three Pillars of Michigan Auto Insurance

Every Michigan auto policy is built on a foundation of three essential coverages. Each one plays a different role in providing financial protection from the various costs that can arise from a car accident.

- Personal Injury Protection (PIP): This is the core of the no-fault system. It covers your medical bills, a percentage of lost income if you are unable to work, and costs for replacement services (such as help with household chores) if you are injured in a crash.

- Property Protection Insurance (PPI): This coverage is unique to Michigan. It provides up to $1 million to pay for damage your car causes to another person’s property within the state, such as buildings, fences, or legally parked vehicles.

- Bodily Injury & Property Damage Liability (BI/PD): This coverage serves as your financial protection if you cause an accident that results in serious injury to someone or damages their vehicle. It is particularly important when driving outside of Michigan, where other states’ at-fault laws apply.

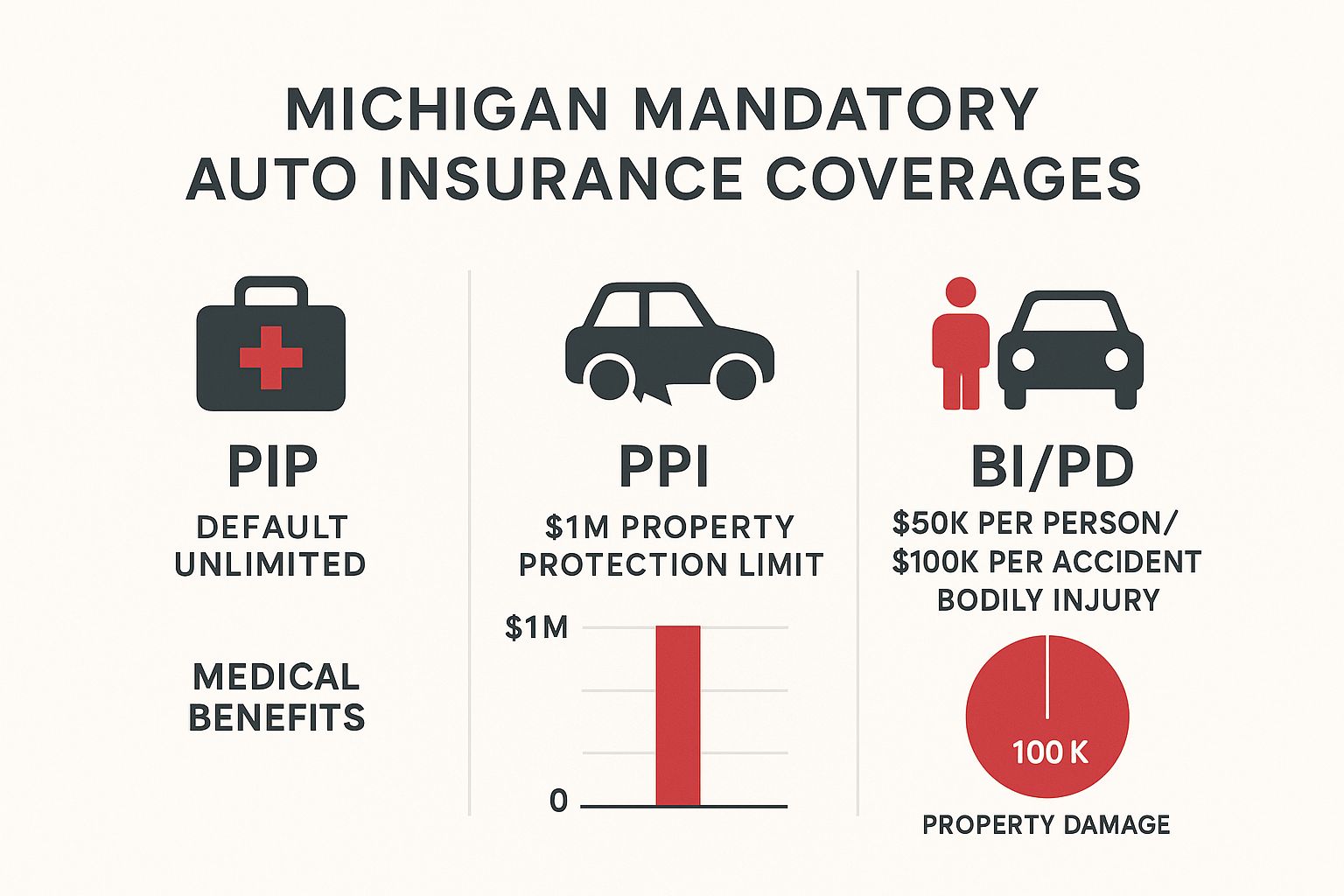

This infographic gives a quick visual breakdown of the minimum limits you’ll need for each of these mandatory coverages.

As you can see, each component addresses a different type of risk, from your own medical care to major property damage. Now, let’s dive deeper into what each of these coverages really means for you.

To make it even clearer, here’s a simple table summarizing the absolute minimums every Michigan driver needs.

Michigan Minimum Auto Insurance at a Glance

This table breaks down the three mandatory coverages required to legally drive in Michigan. While these are the state-mandated minimums, it’s often wise to consider higher limits for better financial protection.

| Coverage Type | State Minimum Requirement | What It Covers |

|---|---|---|

| Bodily Injury Liability (BI) | $50,000 per person / $100,000 per accident (if the driver formally chosen to opt down from the default $250,000/$500,000 coverage.) | Pays for medical costs and other damages if you cause an accident that seriously injures or kills someone. |

| Property Damage Liability (PD) | $10,000 per accident (for out-of-state incidents) | Covers damage your vehicle causes to another person’s property (like their car) in an accident outside of Michigan. |

| Property Protection (PPI) | $1 million per accident (for in-state incidents) | Pays for damage your vehicle causes to property in Michigan, such as buildings, fences, and properly parked cars. |

| Personal Injury Protection (PIP) | Varies by choice, with options ranging from unlimited medical to $50,000 or opting out entirely. | Covers your own medical expenses, a portion of lost wages, and replacement services after an accident, regardless of fault. |

Remember, these are just the starting points. Building the right policy often involves looking beyond the bare minimums to ensure you and your assets are truly protected.

Understanding Personal Injury Protection (PIP)

For drivers in Michigan, Personal Injury Protection, or PIP, is a critical part of an auto insurance policy. It functions as specialized health coverage for injuries sustained in a car accident. Because Michigan is a no-fault state, your own PIP coverage is the primary payer for your medical care, regardless of who caused the crash.

However, PIP is more than a medical plan. It is designed to provide a financial cushion during your recovery.

It also helps cover:

- Up to 85% of lost wages if your injuries prevent you from working, subject to a monthly maximum.

- Up to $20 per day for “replacement services”—a fund to help pay for everyday tasks you cannot perform yourself, like yard work or childcare.

A History of High Costs and Recent Reforms

For years, Michigan residents faced some of the highest auto insurance premiums in the nation. A primary factor was a mandatory unlimited lifetime PIP medical benefit, which had been law since 1973. While this provided extensive care for individuals with catastrophic injuries, it also contributed to Michigan becoming the most expensive state for car insurance.

By 2019, premiums were reportedly 79% higher than the national average. The significant cost of these claims, managed by the Michigan Catastrophic Claims Association, led to major legislative reforms. These reforms changed the landscape of Michigan auto insurance requirements, giving consumers more control over their coverage choices. If you’re curious about the details, you can explore the history of Michigan’s no-fault system to see how these changes came about.

Choosing Your Personal Injury Protection (PIP) Level

The most significant change from these reforms is that you are no longer limited to a single, high-cost PIP option. Today, Michigan drivers can choose a coverage level that aligns with their budget and existing health insurance. This is a critical decision when setting up your policy.

You can now select a coverage amount that fits your needs and budget. Each tier offers a different level of protection, and eligibility for some lower-cost options depends on your existing health plan.

Key Takeaway: Your PIP selection involves a trade-off between your monthly premium and your financial safety net after an accident. Choosing a lower limit can reduce your premium, but it means you will rely more heavily on your personal health insurance—and your own savings—in the event of a serious injury.

To clarify, let’s break down the different PIP medical coverage options now available. This table shows who qualifies for each tier and what it means for your protection.

Choosing Your Personal Injury Protection (PIP) Level

The recent reforms give you several choices for your PIP medical coverage. This comparison should help you understand which options you’re eligible for and how they differ in the amount of protection they offer.

| PIP Coverage Option | Medical Coverage Limit | Who Is Eligible |

|---|---|---|

| Unlimited Lifetime Coverage | Unlimited | All Michigan drivers are eligible for this option, providing the highest level of protection. |

| Up to $500,000 per person/accident | $500,000 | All Michigan drivers are eligible for this option. |

| Up to $250,000 per person/accident | $250,000 | All Michigan drivers are eligible for this default option. |

| Up to $50,000 per person/accident | $50,000 | The applicant must be enrolled in Medicaid, and other household members must have other qualified coverage. |

| Medicare Opt-Out | $0 (relies on Medicare) | The applicant must be enrolled in Medicare Parts A & B, and other household members have qualified coverage. |

Making the right choice here is all about balancing cost with risk. Carefully consider your existing health coverage and financial situation before deciding on a PIP level.

Covering Liability and Property Damage

While Personal Injury Protection (PIP) covers your own medical needs, Michigan law also holds you accountable for damages you may cause to others. This financial responsibility is handled by two separate, mandatory coverages: Property Protection Insurance (PPI) and Bodily Injury & Property Damage Liability (BI/PD).

These coverages function as a financial shield, protecting your personal assets—such as your home, savings, or vehicle—from the high costs of an at-fault accident. Without them, you could be held personally liable for significant expenses.

The Role of Property Protection Insurance (PPI)

Property Protection Insurance is a feature of Michigan’s no-fault system. Its purpose is to pay for damage your vehicle causes to someone else’s stationary property inside Michigan. This includes items like fences, mailboxes, buildings, or a legally parked car.

The state mandates a significant limit for this coverage.

- Coverage Limit: Your policy must include $1 million in PPI coverage.

This high limit exists to cover potentially catastrophic property damage, such as crashing into a commercial building. It is a core piece of the Michigan auto insurance requirements designed to protect property owners throughout the state.

Understanding Bodily Injury and Property Damage Liability (BI/PD)

This coverage applies when you are legally responsible for an accident that seriously injures another person or damages their moving vehicle. It serves as your primary defense against a lawsuit and is particularly crucial when you drive out-of-state, where Michigan’s no-fault rules do not apply.

Michigan sets default minimum liability limits but also allows drivers to select lower limits, a choice that requires careful consideration.

The default minimum liability limits are $250,000 for bodily injury per person and $500,000 per accident. However, drivers can sign a form to select lower limits, with the absolute minimum being $50,000 per person and $100,000 per accident. For property damage in another state, the minimum is $10,000.

Opting for state minimums may leave you financially exposed in a serious accident. Many drivers benefit from considering higher liability limits for added protection, depending on their assets and risk tolerance. Discuss your specific needs with an insurance agent to ensure the coverage you choose matches your circumstances. If you cause an accident resulting in multi-car damage or a permanent disability for another person, the costs could be financially devastating.

For this reason, choosing higher liability limits is a prudent decision for many drivers. It provides a much stronger buffer, safeguarding your financial future from a potential lawsuit. For any driver, including owners of valuable assets like an electric vehicle, strong liability coverage is a necessity for financial security.

How Recent Reforms Impact Your Policy and Wallet

For years, Michigan residents paid some of the highest car insurance premiums in the United States. This was largely due to a system that required every driver to carry unlimited, lifetime Personal Injury Protection (PIP) medical benefits.

While this coverage offered a substantial safety net, it also caused premiums to rise to levels that were difficult for many families to afford. The financial burden and public demand for change eventually led to action.

A landmark legislative overhaul signed into law in 2019 completely rewrote the rules for Michigan auto insurance requirements. The new system moved away from the one-size-fits-all mandate, giving consumers more control over their coverage and costs.

The Shift from Mandate to Choice

The core of the reform is choice, specifically regarding your PIP medical coverage. You are no longer required to purchase the single, expensive unlimited plan. Now, you can select a coverage level that better fits your personal health insurance situation and budget.

This change was driven by data. Between 2000 and 2013, the average cost for PIP coverage in Michigan increased by 278%, even as the number of people injured in accidents declined.

During that period, PIP grew from representing about one-fifth of a total premium to more than half of it, becoming the single biggest driver of high rates. You can read the full analysis on how these costs escalated to see the numbers for yourself.

This new flexibility gives you more control. By carefully reviewing your existing health plan, you have an opportunity to reduce your auto insurance bill, potentially saving hundreds or even thousands of dollars annually.

New Rules to Control Costs

In addition to providing consumer choice, the reforms introduced other measures to address rising expenses. These changes work behind the scenes to help stabilize rates and curb the cost growth seen in previous decades.

Two of the most impactful changes are:

- Medical Fee Schedules: The state established a new fee schedule that places limits on what healthcare providers can charge for services to treat individuals injured in auto accidents. This helps control overbilling and adds consistency to medical costs.

- Fraud Investigation Unit: A dedicated anti-fraud unit was created to investigate and prosecute fraudulent claims and other illegal activities that increase costs for all policyholders.

What This Means for You: These reforms have fostered a more competitive and transparent insurance market in Michigan. While unlimited PIP remains an option for those who want maximum protection, you are now empowered to choose a plan that better suits your life and budget. This is a significant change for all drivers, including EV owners. The potential savings on insurance can help offset the higher purchase price of an electric vehicle, making the total cost of ownership more favorable.

Specialized Coverage For Electric Vehicle Owners

Insuring an electric vehicle in Michigan involves more than meeting state requirements; it involves protecting a sophisticated piece of technology and a significant financial investment. While your EV policy must include PIP, PPI, and liability coverage, a standard policy may not adequately account for the unique components of your electric car.

A generic insurance approach can leave potential coverage gaps. For instance, the high-voltage battery can constitute a large portion of an EV’s total value. In the event of an accident, standard collision or comprehensive coverage might not be sufficient to cover the full cost of repairing or replacing this critical and expensive component.

Protecting Your High-Tech Investment

The primary difference between insuring a conventional gasoline car and an EV lies in the specialized parts and repair expertise required. The battery is a central component, but there are also electric motors, complex software, and other proprietary technologies that require specific protection.

Your policy should address these unique risks directly to avoid unexpected out-of-pocket expenses.

Here are key areas where specialized EV coverage is beneficial:

- Battery and Electric Motor Protection: A policy should ideally cover the full replacement cost of the battery and other core drivetrain components, which can be significantly more expensive than a traditional engine.

- Charging Equipment Coverage: This optional coverage can protect your home charging station or portable charging cables from damage, theft, or power surges.

- Specialized Repair Costs: Repairing an EV requires technicians with specific training and tools, which often results in higher labor rates. A well-designed EV policy will account for these elevated costs.

Finding The Right EV-Specific Policy

Not all insurance carriers have fully adapted to the electric vehicle market. It is important to work with an agent or agency that understands these differences and can find a policy that provides comprehensive protection without being overpriced. The right policy does more than meet the minimum michigan auto insurance requirements; it provides genuine peace of mind.

To better understand EV insurance, it can be helpful to address some of the common myths surrounding electric vehicles.

A well-crafted EV policy is designed to handle specific risks, from battery coverage to protection for your home charging station. It acknowledges that you are insuring a complex piece of modern technology.

Furthermore, many EVs are equipped with Advanced Driver-Assistance Systems (ADAS), which can qualify for significant premium discounts. An experienced agent will know to seek out these savings. For a deeper dive into securing the right coverage, you can review our detailed guide on https://www.evuniverse.com/ev-insurance-michigan/.

A properly structured policy ensures your forward-thinking vehicle is protected by equally forward-thinking insurance.

Finding the Right Michigan Auto Insurance Policy

Shopping for auto insurance in Michigan is not just about meeting legal requirements; it’s about building a protective shield for you and your assets. The process is much smoother when you have all the necessary information ready from the start, helping to ensure the quotes you receive are accurate.

Before you begin shopping for quotes, gather the following information:

- Driver Information: The full name, date of birth, and driver’s license number for every licensed driver in your household.

- Vehicle Information: The Vehicle Identification Number (VIN), make, model, and year for each car you plan to insure.

- Driving History: Be prepared to provide details about any accidents, tickets, or claims for all drivers. Insurers typically review the past three to five years.

Assess Your Personal Coverage Needs

Once your information is organized, think beyond the state minimums. Meeting the michigan auto insurance requirements is the baseline; Your personal finances, health coverage, and driving habits will impact what level of insurance is right for you. Minimum state requirements are a baseline, but additional protection may be appropriate, discuss your options with a licensed agent.

Consider your assets. If you own a home or have savings and investments, higher liability limits are your best defense against a major lawsuit that could put your financial security at risk.

Choosing the right PIP level is another critical decision that should be made in context with your existing health insurance. If you have a high-deductible health plan, for instance, a higher PIP limit could be a financial lifesaver by preventing large out-of-pocket medical bills after a crash. For a deeper dive into crafting a policy from the ground up, feel free to check out our broader guide on auto insurance.

Also consider optional coverages that can provide added peace of mind, such as specialized car key replacement insurance.

An experienced insurance agent can be a valuable resource in this process. They understand Michigan’s complex laws and can help find a policy that fits your specific needs, especially for unique vehicles like EVs. Their expertise helps ensure you obtain a policy that delivers both compliance and security.

Common Questions About Michigan Auto Insurance

When navigating Michigan’s no-fault insurance system, several questions commonly arise. Getting clear answers is the first step toward securing the right protection without overpaying for unnecessary coverage.

One frequent question is whether you still need health insurance if you have unlimited Personal Injury Protection (PIP). The answer is yes. PIP coverage is specifically for injuries sustained in a car accident. It does not cover general illnesses, routine check-ups, or injuries unrelated to a vehicle crash. Your regular health insurance is necessary for all of life’s other medical needs.

Uninsured Drivers and PIP Opt-Outs

Another common concern is what happens if an uninsured driver hits you. Because Michigan is a no-fault state, your own PIP coverage pays for your medical bills up to your policy limit, regardless of who caused the accident. However, PIP does not cover damage to your vehicle. For that, you would need optional collision coverage on your policy.

You might also wonder if it’s possible to opt out of PIP medical coverage entirely. This is possible, but only under very specific circumstances.

To qualify for a complete PIP opt-out, the policyholder must be enrolled in both Medicare Parts A and B. Additionally, every other person in their household must also have their own qualified health coverage.

This is a significant decision that should not be made lightly. It is essential to have a detailed discussion with a licensed insurance professional to confirm eligibility and fully understand the associated risks. The rules surrounding michigan auto insurance requirements are precise, and a misunderstanding can lead to serious consequences. Therefore, we highly recommend to consult a licensed insurance professional to fully understand your eligibility, coverage options, and the associated risks before making coverage selections.

As EVs become more prevalent, it is also wise to see how these rules apply to different makes and models. For example, you can read more about what Tesla insurance rates look like in our other guides. Understanding these details is key to building a policy that provides comprehensive protection.

This article is for general informational purposes only and does not provide legal or tax advice. Coverage options and eligibility vary. Consult a licensed insurance agent for guidance on coverage choices appropriate for your situation.

At EV Universe, we specialize in finding the right coverage for your electric vehicle while meeting all of Michigan’s unique requirements. Get a quote today at https://www.evuniverse.com.