Driving in North Carolina means you have a fundamental responsibility to protect yourself and others on the road. The state enforces this through mandatory auto insurance laws that act as a financial safety net for everyone.

Think of your insurance policy less as a piece of paper and more as a critical tool. It’s what stands between you and a financial catastrophe after a single bad day on the road.

The core principle is straightforward: if you own a vehicle registered in North Carolina, it must have continuous liability insurance. There are no grace periods or exceptions to this rule. The North Carolina Division of Motor Vehicles (NCDMV) electronically monitors this, working directly with insurance carriers to track every policy’s status.

Your Guide to NC Auto Insurance Laws

So, what does a compliant policy actually look like? In North Carolina, it’s built on three essential pillars of coverage. These components work together to cover different angles of a potential accident, ensuring there’s a plan for injuries, property damage, and irresponsible drivers.

The Three Pillars of NC Coverage

Every legally compliant policy in North Carolina must include these three coverages:

- Bodily Injury (BI) Liability: This is the part of your policy that steps in to cover medical bills, lost wages, and other costs for people you injure if you cause an accident.

- Property Damage (PD) Liability: This pays for the repair or replacement of someone else’s property—usually their car, but it could also be a fence or mailbox—that you damage in an at-fault crash.

- Uninsured/Underinsured Motorist (UM/UIM): This is your protection. It covers you and your passengers if you’re hit by a driver who has no insurance or not nearly enough to cover your expenses. It’s a vital safeguard.

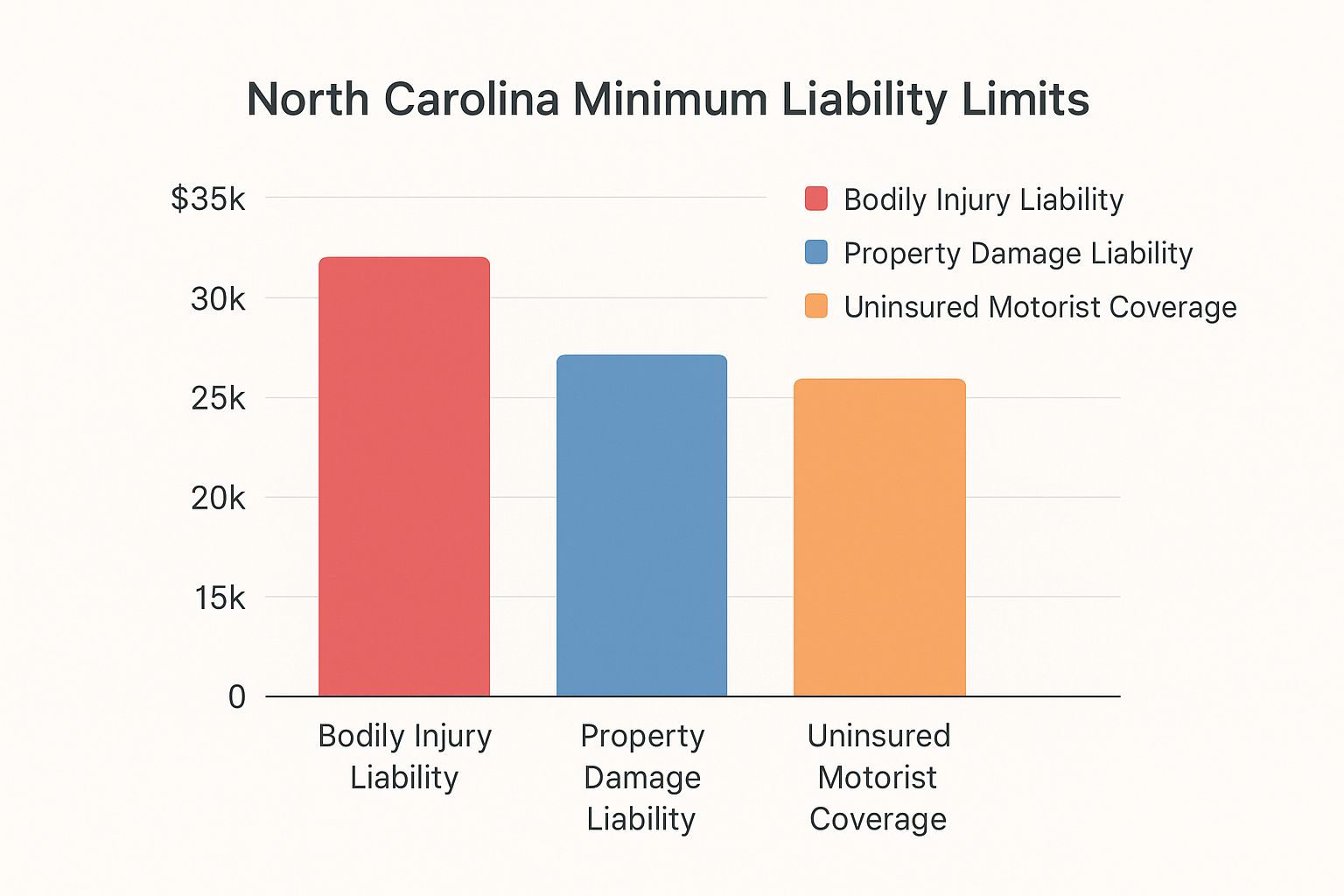

This chart breaks down the minimum liability limits required for each of these core coverages.

As you can see, the state minimums provide a baseline of protection. But with the rising costs of modern vehicles and medical care, these limits can be exhausted quickly in a serious accident.

Why Compliance Matters

Understanding these laws is critical for every driver, whether you’re behind the wheel of a classic sedan or a brand-new electric vehicle. The legal requirements are the same for all vehicle types. However, the higher repair costs associated with the advanced technology in many EVs make robust coverage particularly important. To see how these laws apply specifically to electric cars, check out our in-depth guide on EV insurance in North Carolina.

The consequences for letting your coverage lapse are swift and automatically enforced. The NCDMV can issue fines starting at $50 for a first offense and can even suspend your vehicle’s registration, making it illegal to drive.

Ultimately, staying compliant is about much more than just following the rules. It’s about having the financial backing to handle the unexpected. A solid grasp of North Carolina auto insurance laws is the first step toward responsible driving and genuine peace of mind on the road.

Decoding Your Mandatory NC Insurance Coverage

Trying to make sense of your auto insurance policy can feel like you’re learning a new language. The good news is, it’s much simpler than it looks. Each piece of your required coverage is just a specific tool for handling the financial fallout an accident can leave behind. Think of it as a protective toolkit where every part has a unique, vital job.

To really get a feel for how these pieces fit together, let’s walk through the three coverages every North Carolina driver must have. We’ll use some real-world situations to show you exactly what you’re paying for and why it’s so important.

Bodily Injury Liability: Your Financial Shield

Bodily Injury (BI) liability is the part of your policy that kicks in to protect you financially when you’re at fault for an accident that hurts someone else. This doesn’t cover your injuries—it’s all about paying for the other driver’s and their passengers’ medical bills, lost income, and pain and suffering.

Let’s say you accidentally roll through a stop sign and cause a crash that injures two people in the other vehicle. Your BI coverage steps up to pay for their hospital care, physical therapy, and any wages they lose while they can’t work. Without it, you could be sued personally for those expenses, putting everything you own on the line.

Property Damage Liability: Protecting Other People’s Stuff

Just like BI, Property Damage (PD) liability covers costs you’re responsible for, but it’s for physical property instead of people. This is what pays to repair or replace the other person’s car when you cause an accident.

And it goes beyond just other cars. If you swerve and take out a homeowner’s fence, flatten a mailbox, or even clip the side of a building, your PD liability is what pays those repair bills. It’s the coverage that keeps a simple driving mistake from becoming a five-figure headache.

Key Takeaway: Both BI and PD liability are there to cover damages you cause to other people. They are the foundation of your responsibility as a driver, making sure victims of an accident are made whole without you facing financial disaster.

North Carolina’s insurance system is built on this foundation. We operate under what’s known as an “at-fault” or “tort” system. This means the driver who is determined to have caused the crash is responsible for paying the damages. That makes your liability coverage absolutely critical.

To help you visualize exactly what’s required, here’s a quick breakdown of North Carolina’s mandatory coverages and the minimum limits that will be in effect starting in 2025.

Mandatory Auto Insurance Coverages in North Carolina

| Coverage Type | What It Covers | Minimum Required Limits (as of Jan 1, 2025) |

|---|---|---|

| Bodily Injury Liability | Pays for injuries to other people in an accident you cause. | $50,000 per person / $100,000 per accident. |

| Property Damage Liability | Pays for damage to another person’s property (like their car or a fence) in an accident you cause. | $50,000 per accident. |

| Uninsured/Underinsured Motorist | Pays for your injuries and property damage if you’re hit by a driver with no insurance or not enough insurance. | Must match your chosen Bodily Injury and Property Damage liability limits. |

These are just the legal minimums. As you can see, the costs from a serious accident can easily exceed these amounts, which is why many drivers opt for higher limits to better protect their assets.

Uninsured And Underinsured Motorist Coverage

While liability coverage has your back when you’re at fault, Uninsured/Underinsured Motorist (UM/UIM) coverage is your personal safety net. This required coverage protects you, your family, and your passengers if you’re hit by a driver who broke the law and has no insurance—or not enough to cover your bills.

Here’s how it plays out:

- Uninsured Motorist (UM): You’re rear-ended by a driver who has no insurance at all. Your UM coverage will step in and pay for your medical bills and other expenses, up to your policy limits, just like their insurance should have.

- Underinsured Motorist (UIM): You get hit by a driver who causes $75,000 in medical bills for you, but they only carry the minimum BI liability limit. Their policy pays out its maximum, and then your UIM coverage kicks in to help cover the rest.

This coverage is a must-have for every driver, but it’s especially important if you own an electric vehicle (EV). EVs often have higher repair costs due to specialized components like battery packs and advanced sensors. Having solid UM/UIM limits ensures you have enough coverage to repair your vehicle, even if the at-fault driver was underinsured.

Finally, while knowing your coverage is key, it’s also wise to understand your rights. Occasionally, you might run into issues with an insurer not handling a claim correctly. Being aware of what constitutes bad faith insurance practices helps ensure you get the full benefits you’re entitled to under your policy.

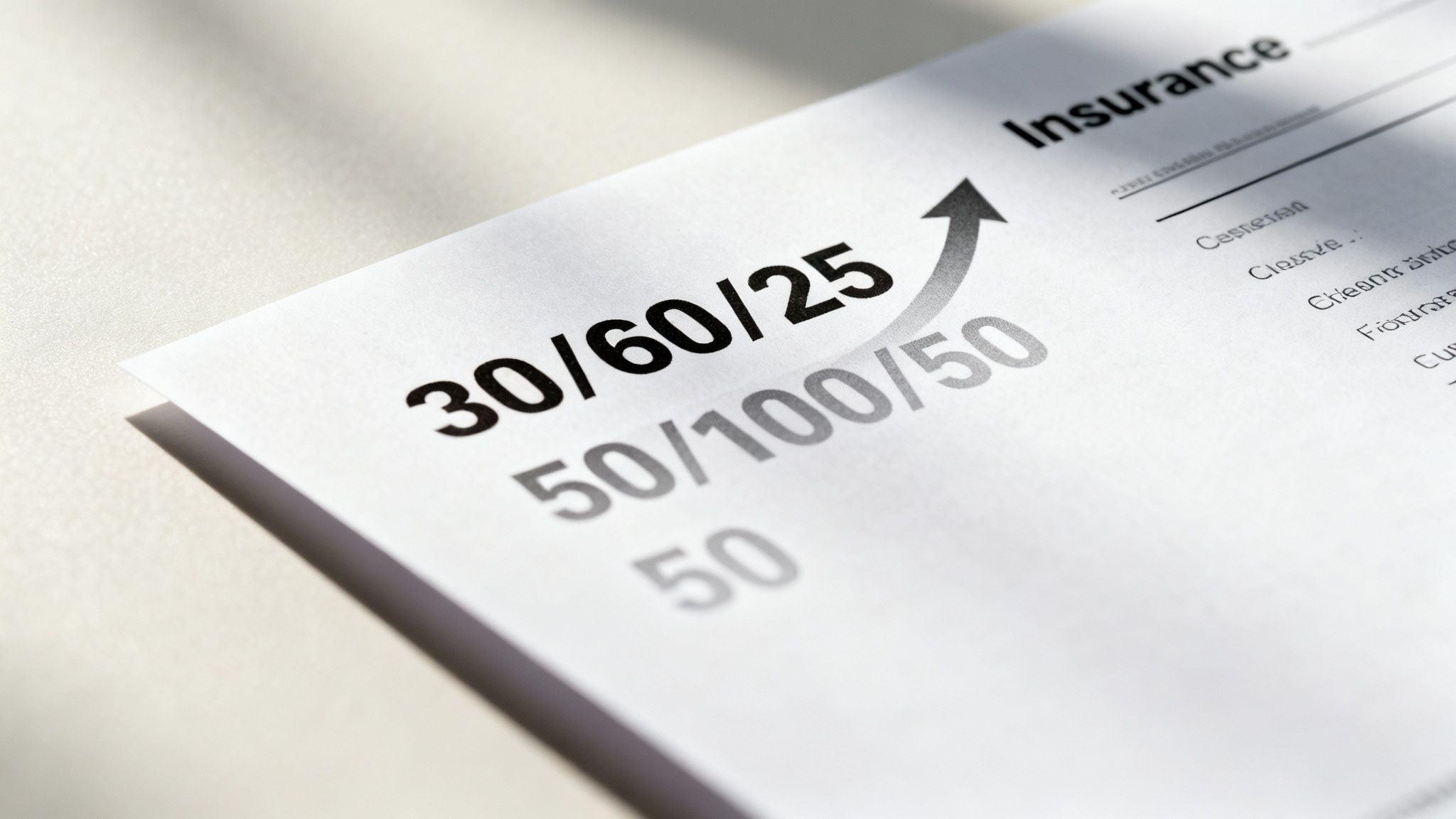

Understanding North Carolina’s New Liability Limits

If you’ve ever squinted at your auto insurance policy, you’ve probably seen a string of numbers like 30/60/25. This isn’t just industry jargon; it’s the bedrock of your liability protection. For years, those numbers were the absolute minimum every North Carolina driver had to carry, but times—and costs—have changed.

Recognizing that these limits were no longer adequate to cover costs in a serious accident, the state legislature acted to provide a more realistic financial safety net, bringing North Carolina auto insurance laws in line with today’s economic realities.

The result is Senate Bill 452, landmark legislation that significantly increases the state’s minimum liability requirements for the first time since 1999.

A New Standard of Protection

Starting July 1, 2025, the mandatory minimums for all drivers in North Carolina will increase substantially. The state legislature passed Senate Bill 452, signed into law in October 2023, to increase liability limits to $50,000 per person and $100,000 per accident for bodily injury, and $50,000 for property damage.

This represents a 67% increase in per-person bodily injury coverage and a 100% increase in the property damage minimum. It’s a clear legislative response designed to provide better financial protection for everyone on the road. You can get more details on these big changes coming to NC auto insurance and what they mean for you.

This isn’t just a small tweak; it’s a fundamental shift in the level of financial responsibility required on North Carolina roads.

The New Minimums Explained:

- $50,000 (Bodily Injury per Person): The most your insurance will pay for a single person’s injuries in an at-fault accident.

- $100,000 (Bodily Injury per Accident): The total amount your insurance will pay for all injuries combined in a single at-fault accident.

- $50,000 (Property Damage per Accident): The max your policy will cover to repair or replace someone else’s property, like their car, a mailbox, or a storefront.

This new standard is often just called 50/100/50 coverage.

Old Limits vs. New Limits: A Real-World Scenario

To see why this change is so important, let’s put the old and new limits to the test in a realistic situation. Imagine you cause an accident that seriously injures one person and totals their brand-new electric SUV.

Scenario with Old Limits (30/60/25):

- Medical Bills: The other driver’s medical costs hit $45,000. Your policy only covers up to $30,000, leaving you personally responsible for the remaining $15,000.

- Vehicle Damage: The EV, with its specialized battery and sensors, costs $40,000 to replace. Your policy’s property damage limit is just $25,000. You are now responsible for another $15,000.

- Total Out-of-Pocket Cost to You: $30,000.

An accident like this could lead to wage garnishment, asset seizure, and significant financial hardship. The old limits were insufficient for modern costs.

Scenario with New Limits (50/100/50):

- Medical Bills: The $45,000 in medical expenses is fully covered by your new $50,000 per-person limit.

- Vehicle Damage: The $40,000 to replace the EV is also completely covered by the new $50,000 property damage limit.

- Total Out-of-Pocket Cost to You: $0.

The new limits provide a much stronger financial shield. This change acknowledges the rising cost of healthcare and the fact that modern vehicles—especially advanced EVs—are more expensive to repair or replace. While the new state minimum is a significant improvement, these rising costs are why many drivers choose even higher limits for more comprehensive protection.

How North Carolina Insurance Rates Are Set

Ever wonder where your car insurance premium comes from? In North Carolina, it’s a regulated process that blends statewide rules with your personal details to determine a final rate. The North Carolina Rate Bureau proposes rates, which are then subject to approval by the Commissioner of Insurance.

The state sets the baseline, but your individual risk factors heavily influence the final premium. Insurers use these factors to predict the likelihood of you filing a claim.

The Role of Your Driving Record

Your driving history is a major factor. North Carolina uses a specific system called the Safe Driver Incentive Plan (SDIP) to standardize how driving violations impact insurance rates.

The plan assigns points for moving violations and at-fault accidents. Drivers with clean records receive the lowest rates, while riskier drivers pay more. The more points you accumulate, the larger the surcharge on your premium.

For example, a conviction for speeding more than 10 mph over a 55 mph speed limit results in 4 insurance points, according to the North Carolina Department of Insurance. This can increase your premium by 80%.

The SDIP creates a clear financial link between your actions behind the wheel and your insurance costs. A clean record is the most effective tool for keeping premiums low.

Key Factors That Shape Your Premium

In addition to your driving record, insurers analyze other data to build a complete risk profile. Some of these are within your control, while others are based on demographics and location.

Here are a few of the most common factors:

- Your Location: Where you live and park your car matters. Urban areas with higher traffic density, accident rates, and vehicle theft statistics typically have higher premiums than rural areas.

- Your Age and Driving Experience: Actuarial data consistently shows that younger, less experienced drivers are involved in more accidents. Consequently, they face higher insurance rates until they establish a long-term safe driving record.

- Annual Mileage: The more miles you drive, the greater your exposure to risk. A long daily commute generally results in a higher premium compared to driving limited annual miles.

- Credit History: In North Carolina, insurers are permitted to use a credit-based insurance score as one of many factors in setting rates. A strong credit history is often seen as an indicator of financial responsibility, which can lead to lower premiums.

Each of these elements helps the insurance company calculate a rate that reflects your specific risk profile.

How Your Vehicle Type Impacts Rates

The car you drive significantly influences your insurance premium. Insurers evaluate the vehicle’s value, typical repair costs, safety ratings, and theft frequency. A high-performance sports car will almost always cost more to insure than a standard family sedan.

This is where the unique characteristics of electric vehicles (EVs) come into play.

The EV Insurance Equation:

It is a fact that EVs can have higher repair costs. Specialized components like high-voltage batteries and advanced driver-assistance systems (ADAS) require technicians with specific training, which can increase the cost of a claim.

However, that is not the complete picture. The advanced safety features common in EVs, such as automatic emergency braking and sophisticated collision avoidance systems, can prevent accidents from occurring. Furthermore, the low center of gravity in many EVs improves handling and stability. Many insurance carriers recognize these benefits and offer discounts for these safety technologies. The world of auto insurance is adapting to these new vehicle dynamics. While repair costs are a valid consideration, the advanced safety and performance of an EV often balance the scale, leading to competitive premiums from insurers who understand this technology.

How to Stay Compliant and Avoid Penalties

Knowing North Carolina’s auto insurance laws is half the battle; staying compliant is the other. The state requires continuous coverage and uses a connected system to enforce this rule.

Here’s how it works: the North Carolina Division of Motor Vehicles (NCDMV) is linked electronically with all licensed insurance carriers. When a policy is canceled or lapses, the insurer is legally required to notify the DMV. This automated process means the state is aware of an uninsured vehicle almost immediately.

This notification triggers an official letter, a Liability Insurance Termination Notification, which is mailed to your address. This is a final warning to resolve the issue promptly.

The Cost of a Coverage Lapse

Ignoring this notice leads to fines and administrative problems. North Carolina’s penalties for driving without insurance are applied automatically and increase with the duration of the lapse and the number of offenses.

A lapse in coverage initiates a civil penalty. For a first offense, the fine is $50. A second lapse within three years increases the fine to $100, and any subsequent lapse is $150. Failure to pay the fine will result in the suspension of the vehicle’s registration.

This means your license plate is revoked, and it becomes illegal to drive the vehicle. To reinstate the registration, you must pay all outstanding fines, a service fee, and provide proof of a new, valid insurance policy.

Your Proof of Insurance: The FS-1 Form

So, how does the state know you’re covered again? When you purchase a new policy or reinstate an old one, your insurance company files a Certificate of Insurance, known as Form FS-1, directly with the NCDMV.

You do not handle this form yourself. Your insurer transmits it electronically, officially certifying to the state that your vehicle meets all legal insurance requirements. If you receive a lapse notice but believe you are covered, contact your insurance agent immediately. They can verify that the FS-1 was filed and help resolve any discrepancies. An experienced agent is crucial, especially for modern vehicles. Our team provides expert guidance on EV insurance in Raleigh, North Carolina, making sure you’re always compliant.

The Right Way to Cancel Your Coverage

Avoiding penalties requires not only timely premium payments but also proper policy cancellation. This is a common point of error for drivers. You can only cancel your insurance after you have officially surrendered your license plate to the NCDMV.

Do not simply call your insurer to cancel a policy for a vehicle you sold or if you moved out of state. As long as the license plate is active in the DMV’s system, you are legally required to maintain liability coverage on it. Turning in the plate first severs that legal obligation and is the only correct way to end your insurance requirement without facing a penalty.

Got Questions About NC Auto Insurance Laws? We’ve Got Answers.

When you get down to the nitty-gritty of North Carolina auto insurance laws, a few common questions always seem to pop up. Let’s break down some of the most frequent scenarios drivers run into and give you straight, practical answers.

What Happens If an Uninsured Driver Hits Me in NC?

If you are hit by a driver who has no insurance, your own policy is your first line of defense. This is precisely why North Carolina requires Uninsured Motorist (UM) coverage.

You will file a claim directly with your own insurance company. Your insurer will cover your medical expenses and vehicle damage up to the limits you selected for your policy. The process requires you to demonstrate to your insurer that the other driver was at fault and was uninsured. If you’re curious about how they figure out what your damaged car is worth, understanding auto insurance appraisals is a great way to get clarity on that crucial step.

Is It More Expensive to Insure an EV in North Carolina?

The cost to insure an EV depends on several factors. On one hand, some carriers may quote higher premiums because EVs have specialized parts, like batteries and advanced sensors, that can be expensive to repair.

However, that is not the full story. Most EVs are equipped with advanced safety features—such as automatic emergency braking and sophisticated collision avoidance systems—that may qualify for significant discounts. The final premium depends on the specific insurer and the EV model. Insurance companies that specialize in EVs often provide more competitive rates because they accurately weigh the benefits of these advanced safety features against potential repair costs, viewing them as a lower overall risk.

Do I Need to Tell the DMV I Switched Insurance Companies?

No, you do not need to contact the NCDMV yourself. When you purchase a new policy, your new insurance company is required by law to handle the notification. They will electronically file a Form FS-1 with the state, certifying that you are covered.

Your critical responsibility is to ensure there is absolutely no gap in coverage. Your new policy must be active the moment your old policy ends. Even a single day of lapse will be flagged by the DMV’s automated system and result in fines and penalties.

At EV Universe, we understand the intricacies of insuring all vehicle types, from the latest electric models to traditional gas-powered cars. We know the factors that determine your rates and specialize in finding policies that provide robust protection at a competitive price. Start your free quote today.