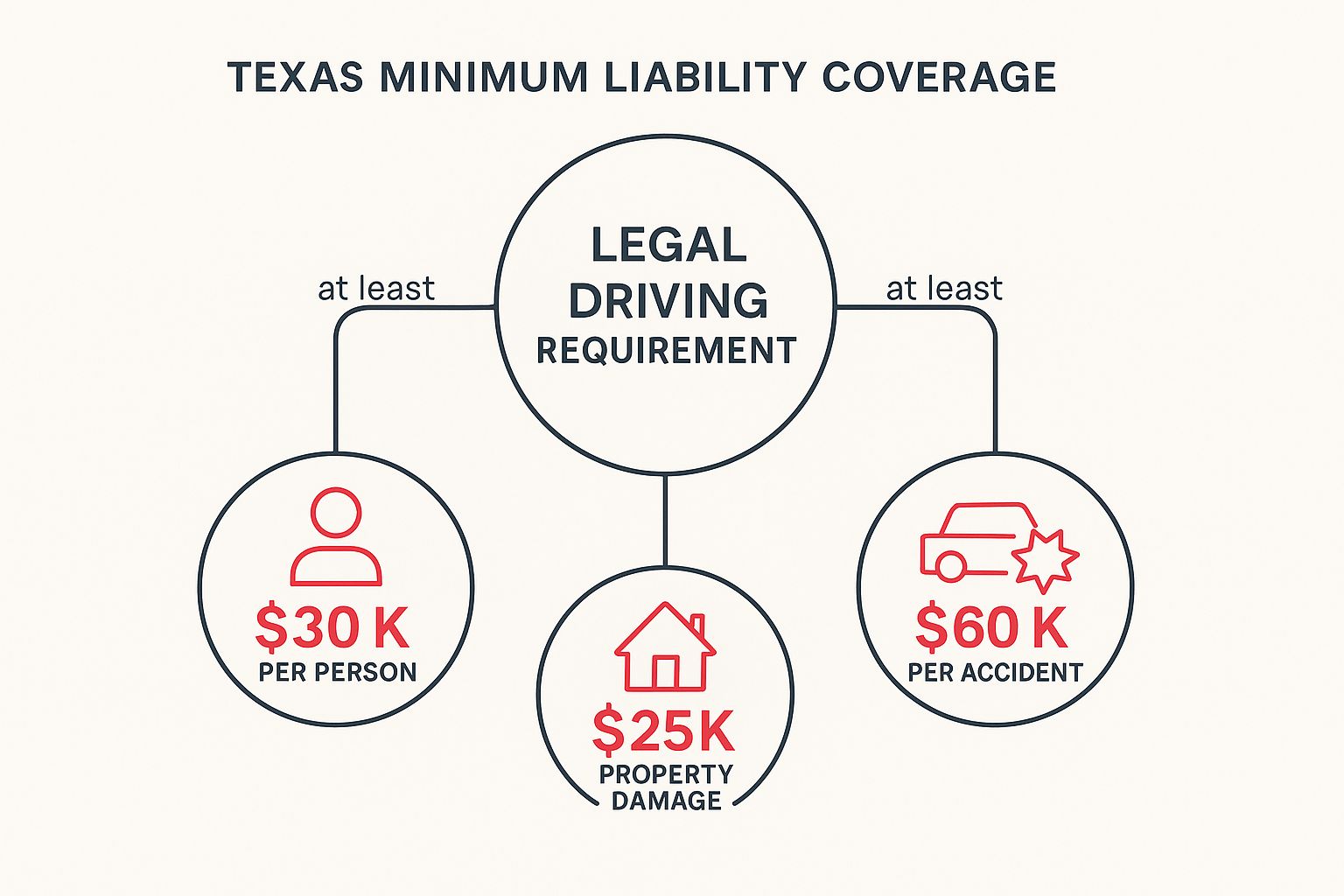

In Texas, driving legally means carrying at least 30/60/25 liability insurance. This isn’t just a random string of numbers; it’s the state-mandated minimum that covers $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. This is the absolute baseline required to get behind the wheel on Texas roads.

The Foundation of Texas Auto Insurance Requirements

Jumping into the world of car insurance can feel like trying to learn a new language, but the core idea is actually pretty simple. In Texas, the law requires every driver to prove they can pay for accidents they cause. For most people, the easiest way to do that is by buying liability auto insurance.

Think of this required coverage as a basic financial safety net. It’s not designed to protect you, but rather the other people you might injure or whose property you might damage if you’re at fault in a crash. It ensures that if you cause a wreck, there’s money available to help the other party recover, protecting them from shouldering the full cost of your mistake.

Breaking Down the 30/60/25 Rule

Texas has required drivers to carry this specific level of liability coverage, known as 30/60/25, for a long time. It sets the minimum dollar amounts your insurance company will pay out if you cause an accident.

Here’s a quick look at what those numbers mean in the real world:

- $30,000 in Bodily Injury Liability (BI) per person: This is the maximum your policy will pay for a single person’s medical bills and related costs if you’re at fault.

- $60,000 in Bodily Injury Liability (BI) per accident: This is the total cap your insurance will pay for all injuries in a single accident you cause, no matter how many people are hurt.

- $25,000 in Property Damage Liability (PD) per accident: This covers the cost of fixing or replacing the other person’s stuff you damaged, like their car, a fence, or a mailbox.

To give you a clearer picture, here’s a quick summary table.

Texas Minimum Liability Coverage At a Glance

The table below breaks down the 30/60/25 rule into its three core components, showing exactly what each part covers and the minimum amount required by law.

| Coverage Type | Minimum Required Amount | What It Covers |

|---|---|---|

| Bodily Injury Liability (Per Person) | $30,000 | Medical expenses for one person injured in an at-fault accident. |

| Bodily Injury Liability (Per Accident) | $60,000 | Total medical expenses for all people injured in an at-fault accident. |

| Property Damage Liability (Per Accident) | $25,000 | Repair or replacement costs for the other party’s damaged property. |

This structure ensures that there’s a basic level of financial protection in place for anyone involved in an accident.

The infographic below really helps visualize how these three distinct coverages come together to create the state’s mandatory protection standard.

As you can see, getting a handle on these basics is the first real step to building a solid insurance policy that keeps you legal and protected.

You must carry proof of this coverage with you anytime you drive. A digital copy on your phone is legally acceptable in Texas. If you can’t show it when asked, you could face hefty fines and penalties. While meeting this minimum is required, it’s worth asking yourself if it’s truly enough to protect your own assets.

For a deeper dive into all your policy options, check out our comprehensive guide on auto insurance.

Why Minimum Coverage Is A Financial Gamble

Carrying the state-mandated 30/60/25 coverage makes you legal to drive on Texas roads. But it’s critical to understand that “legal” is a long way from “financially safe.” Think of the Texas auto insurance requirements as the absolute floor—not a comprehensive shield. Relying only on these bare-bones limits is a significant financial gamble if you’re ever in a serious accident.

When the costs from an accident exceed your policy limits, you are personally responsible for every dollar of the difference.

The Staggering Cost of Modern Accidents

Let’s be factual: $25,000 for property damage doesn’t go as far as it used to. According to Kelley Blue Book, the average price of a new car in the U.S. surpassed $47,000 in late 2023. Totaling just one other new vehicle could leave you with a $22,000 bill after your insurance has paid its maximum. This is a massive risk, especially when electric vehicles are involved. While EVs often feature advanced safety systems, their high-tech components and specialized batteries can lead to higher repair or replacement costs in the event of a severe accident.

A multi-car pileup on a congested highway like I-35 in Austin or I-45 in Houston paints an even more serious picture.

Picture this: you cause an accident involving three other cars. Even if the damage to each is only moderate, the total could easily rocket past your $25,000 property damage limit. Suddenly, you’re left paying the remaining repair bills for two of those cars entirely out of your own pocket.

It’s the same story with medical bills, which can escalate quickly. If you injure two people and their combined medical expenses hit $100,000, your $60,000 per-accident limit for bodily injury is exhausted. That leaves a $40,000 shortfall that the injured parties can pursue you for. This could lead to having your wages garnished or even liens being placed against your home.

Texas-Specific Risks That Up the Ante

Driving in Texas comes with its own unique set of challenges that make higher coverage limits a much smarter financial move. The state’s sprawling cities are famous for bumper-to-bumper traffic, making multi-vehicle accidents a daily occurrence. And once you get outside the city limits, you have to contend with unpredictable weather.

Keep these factors in mind:

- Hailstorms: Severe hail can damage dozens of cars in minutes. If you cause a wreck during such an event, the property damage costs can stack up quickly.

- High-Value Vehicles: From luxury SUVs in Dallas to massive pickup trucks in West Texas, you’re sharing the road with plenty of vehicles that cost way more than your $25,000 property damage limit.

- Urban Congestion: Major hubs like Dallas and Houston have some of the most intense traffic in the country, which means accidents are not just more frequent, but often far more complex.

At the end of the day, treating your insurance policy as just a box you have to check is a risky bet. A solid policy isn’t just an expense; it’s a strategic tool designed to protect your assets and your financial future from the chaos of the open road.

Key Optional Coverages For Real-World Protection

While state-mandated liability insurance takes care of the other person’s damages, it does absolutely nothing for your own car, your medical bills, or the mess left behind by an uninsured driver. While meeting the legal minimum is a good start, many drivers may want to consider higher coverage limits to better protect their assets and financial well-being, depending on their individual needs and circumstances.

Adding these optional coverages is the difference between simply being legal and having genuine peace of mind every time you get behind the wheel. Let’s break down the key protections you need to handle Texas’s most common—and costly—roadside risks.

Protecting Your Own Vehicle

Two of the most important add-ons you can get are Collision and Comprehensive coverage. They’re a dynamic duo that covers physical damage to your car, but they each tackle completely different scenarios.

- Collision Coverage: This pays for damage to your car resulting from a collision with another object. Think about backing into a pole or being in an accident where you were deemed at fault. Collision pays to get your car fixed.

- Comprehensive Coverage: Often called “other than collision,” this is for damage from non-driving events. This is a big one here in Texas, where the unexpected is common.

Comprehensive coverage is what kicks in when a sudden hailstorm damages your car or a deer sprints across a Hill Country road at the worst possible moment. It also has your back in cases of fire, vandalism, and theft.

Here’s a dose of Texas reality: According to the National Insurance Crime Bureau, Texas had the second-highest number of vehicle thefts in the nation in 2022. That, combined with our state’s propensity for severe weather, means comprehensive claims are a frequent occurrence. If you explore more data on Texas auto insurance trends, you’ll quickly see why this coverage is a must-have.

Shielding Yourself From Others

Even if you have a good policy, you can’t control what other drivers do. And unfortunately, a surprising number of Texans drive with either no insurance or not nearly enough. This is where a couple of other coverages become your personal financial bodyguards.

Uninsured/Underinsured Motorist (UM/UIM) Coverage is your best defense against irresponsible drivers. If someone with no insurance hits you and causes injuries, UM coverage steps in to handle your medical bills and lost wages. In the same vein, UIM fills the gap when the at-fault driver has insurance, but their policy limits aren’t enough to cover your expenses.

On top of that, optional Personal Injury Protection (PIP) is an absolute gem in Texas. It helps pay for your medical bills and lost wages after a wreck, no matter who was at fault. That means you can get immediate financial help for your injuries without having to wait weeks or months for the insurance companies to finish determining fault.

To make sense of it all, it helps to see these coverages laid out side-by-side.

Key Optional Insurance Coverages Compared

Here’s a quick comparison of these essential optional coverages and the specific risks they protect you from as a Texas driver.

| Coverage | What It Protects You From | Why It’s Important in Texas |

|---|---|---|

| Collision | Damage to your own vehicle from a collision with another car or object (e.g., pole, fence). | Covers you in at-fault accidents and hit-and-runs in crowded urban parking lots or busy highways. |

| Comprehensive | Damage to your vehicle from non-collision events like theft, vandalism, fire, hail, or hitting an animal. | Essential for Texas’s notorious hailstorms, high auto theft rates, and abundant wildlife. |

| UM/UIM | Your medical bills and lost wages when you’re hit by a driver with no insurance or too little insurance. | Protects you from the financial fallout of being hit by one of Texas’s many uninsured drivers. |

| PIP | Your medical bills and lost wages after an accident, regardless of who is at fault. | Provides immediate financial relief for injuries without waiting for a lengthy fault investigation. |

Ultimately, layering these protections on top of your basic liability policy is what creates a truly comprehensive shield against the financial risks of driving in Texas.

Special Insurance Needs For Texas EV Owners

Getting insurance for an electric vehicle in Texas isn’t just about checking a box to meet the state’s basic auto insurance requirements. EVs are a serious investment, packed with unique parts and technology that a standard, gas-car policy may not be built to fully protect.

The heart of an EV is its high-voltage battery. If that gets damaged in a wreck, the replacement cost can be substantial. The wrong collision policy might leave a gap between the payout and the actual cost.

And don’t forget about your home charging station. Your standard homeowner’s policy may offer limited protection for these units. Speak with your insurance agent to make sure you are fully covered.

Factoring in Advanced Technology and Repair Costs

Today’s electric cars are essentially computers on wheels. They’re loaded with sophisticated software, sensors, and driver-assist systems that make them safer but also complicate post-accident repairs.

Fixing an EV isn’t a job for just any mechanic. It often requires technicians with specialized training and proprietary diagnostic tools, which can drive up labor costs. Looking into things like EV maintenance costs helps paint a clearer picture of why insurance premiums can look different for electric models. Insurers must account for potentially higher repair bills when they calculate rates.

It’s a common misconception that EVs are always more expensive to insure. While repair costs are a factor, many EVs come equipped with advanced safety features like automatic emergency braking and lane-keeping assist, which can qualify for significant discounts and help offset the premium.

Finding the Right Coverage for Your EV

Because EVs have such distinct needs, it’s incredibly important to work with an agent who understands the technology. An expert can help you pinpoint a policy that gives you the right protection without making you overpay. For a deeper dive, you can learn more about securing the best EV insurance in Texas and make sure your investment is properly covered.

When you talk to your agent, make sure to bring up these key coverages areas and potential discounts:

- EV Battery : This can help cover the high cost of replacing the battery, the single most expensive component.

- Charging Equipment Protection: Adds a layer of security for your home charging station.

- Original Equipment Manufacturer (OEM) Parts: Guarantees that any repairs use factory-approved parts, maintaining your car’s integrity.

- Safety Feature Discounts: You could get savings for features like automatic emergency braking or lane-keep assist.

- Eco-Friendly Discounts: Some carriers will actually give you a better rate just for driving an electric car.

By focusing on these specific areas, you can build an insurance plan that truly reflects the reality of owning and driving an EV in Texas.

What To Do When You Need An SR-22

Getting hit with an SR-22 requirement can feel like a major setback, but it’s a much more manageable process than most drivers realize. Let’s clear up a common misconception right away: an SR-22 isn’t actually an insurance policy. It’s just a certificate your insurance company files with the state for you.

Think of it as a note from your insurer to the Texas Department of Public Safety. This note guarantees that you’re carrying at least the minimum liability coverage the law requires, confirming you’re financially responsible and legal to be on the road.

Common Reasons for an SR-22 Filing

Usually, an SR-22 comes into play after a serious driving violation that gets you flagged as a higher-risk driver. While every case is different, the state typically requires this filing for a few specific offenses.

Here are some of the most common triggers:

- Driving While Intoxicated (DWI) or Driving Under the Influence (DUI)

- Getting into an accident while you were uninsured

- Racking up multiple traffic tickets in a short time frame

- Driving with a suspended or revoked license

These violations tell the state that your driving habits need extra supervision. The SR-22 is how they monitor you, making sure you keep your insurance coverage active without any gaps. If you’re dealing with a specific conviction, it’s smart to understand all the potential consequences, from insurance rate hikes and SR-22 requirements, to stay ahead of the game.

How to Get an SR-22

Getting an SR-22 is a pretty straightforward, step-by-step process. The first thing you need to do is tell your insurance provider you need one. Not all companies offer SR-22 filings, so you might have to shop around for a new insurer who can handle it.

Once you find a provider who can help, they’ll usually charge a small filing fee, typically around $25, to send the form to the state. Your insurer takes care of all the paperwork, certifying that your policy meets all Texas auto insurance requirements.

Here’s the critical part: you absolutely must maintain your policy without any breaks. If your coverage gets canceled for any reason, your insurer is legally required to notify the state immediately. That would land you right back with a suspended license.

Having to file an SR-22 can actually be a good time to take a fresh look at your coverage. Our experts can walk you through different options to find a policy that fits your new situation, even with this requirement on your record. You can learn more about our approach to personal insurance solutions designed to keep you protected.

Ever wonder who keeps insurance companies in check? In Texas, that job falls to the Texas Department of Insurance (TDI). Think of them as the state’s official consumer protection agency, acting as a referee to make sure every insurance company plays by the rules and treats you fairly.

The TDI has been looking out for Texas consumers for a long time. While regulation started way back in 1910, the modern version of the agency really took shape in 1991. This was a huge turning point, forcing insurers to set up toll-free lines for complaints and offer policy info in both English and Spanish—a major boost for consumer rights. You can dive deeper into the TDI’s history and its consumer protection mission to see just how much its role has grown.

That commitment to protecting you is stronger than ever today, and the TDI handles several critical functions that have a direct impact on your auto policy.

What Does The TDI Actually Do?

At its core, the TDI’s mission is to regulate the insurance industry and protect you, the consumer. This breaks down into a few key jobs:

- Licensing and Monitoring: Before an insurance company can even sell a policy in Texas, they have to get a license from the TDI. The agency also keeps a close watch on their financial stability to make sure they actually have the money to pay out claims when you need it.

- Policy Review: The TDI reviews the fine print on insurance policies before they’re sold. They’re looking to make sure the language is clear, fair, and follows all the state laws. No hidden “gotchas.”

- Consumer Assistance: This is a big one. If you run into a dispute with your insurer or just feel like you’re being treated unfairly, the TDI’s Help Line is an incredible resource. They can step in, answer your questions, and even launch an investigation on your behalf.

The TDI is your advocate in the insurance world. If you have a question or a problem with a claim, give their Help Line a call at 800-252-3439 for some expert backup.

Knowing that a powerful regulatory body is overseeing Texas auto insurance requirements should give you some peace of mind. It’s a good reminder that the system is designed to protect you, which is exactly why we’re committed to operating with total transparency within those same guidelines.

Common Questions About Texas Auto Insurance

Diving into the world of auto insurance can feel like opening a can of worms, with tons of “what if” scenarios popping into your head. Getting straight answers is the only way to feel truly confident when you get behind the wheel. Let’s tackle some of the most common questions we hear about Texas auto insurance.

What Happens If I Drive Without Insurance In Texas?

Driving without proof of financial responsibility is a serious offense in the Lone Star State.

For a first-time violation, you’re looking at fines anywhere from $175 to $350, plus court costs. If it happens again, the penalties get much more severe. We’re talking fines up to $1,000, a suspended driver’s license, and even having your vehicle impounded. On top of all that, you’ll almost certainly be required to file an SR-22 certificate to get your driving privileges reinstated.

Does My Texas Insurance Cover Me In Other States?

Yes, your Texas liability policy travels with you across the United States and into Canada.

Your coverage automatically adjusts to meet the minimum liability requirements of any state or province you’re driving through. So, if you cross into a state with higher minimums than Texas, your policy temporarily bumps up your protection to match their laws. No need to buy a separate policy just for a road trip.

In Texas, auto insurance is designed to follow the vehicle, not just the driver. This principle, known as “permissive use,” means your policy’s liability, collision, and comprehensive coverages typically extend to an accident if you’ve given someone permission to borrow your car.

Do I Need Special Insurance For Ridesharing?

You absolutely do. This is a big one that catches a lot of people off guard. Your standard personal auto policy has a very specific exclusion for any commercial activity, and that includes driving for services like Uber or Lyft.

If you get into an accident while you’re “on the clock” for a rideshare app, your personal insurer can flat-out deny the claim. That would leave you on the hook for everything. To be covered properly, you have to tell your insurance company and add a specific rideshare endorsement to your policy, or in some cases, get a separate commercial auto policy.

Coverage options and needs vary for each driver and household. For precise recommendations, speak directly with a licensed insurance professional.

At EV Universe, our job is to find the right answers and the right coverage for all Texas drivers, whether you’re behind the wheel of an EV or a gas-powered car. We specialize in making the complex Texas auto insurance requirements easy to understand.